The App Era Is Ending

Open your phone and count the finance apps. Your bank. Your crypto wallet. Your remittance app. Your budgeting tool. Your payment processor.

Five icons. Five passwords. Five separate interfaces.

Now ask yourself something uncomfortable:

Why does moving your own money require launching a separate app at all?

For a decade, fintech innovation meant building more apps. Better dashboards. Cleaner interfaces. Faster logins. But the model never changed. Finance lived in its own box, a standalone destination you had to consciously open.

In 2026, that model is collapsing. Finance is no longer a place you go.

It’s becoming something that happens inside conversations, inside AI assistants, and inside the platforms you already use daily.

Apps are disappearing, and invisible finance is rising.

What Is Invisible Finance?

Invisible finance refers to financial services that operate seamlessly within existing digital environments instead of requiring standalone banking applications.

Instead of:

- Opening a bank app

- Filling out transfer forms

- Switching between payment tools

You simply type:

“Send $200 to Mom.”

And it happens.

Invisible finance is powered by:

- Embedded payments

- AI-driven financial assistants

- Messaging-platform integrations

- Identity-based security layers

- Real-time conversational interfaces

This shift represents one of the most important fintech trends of 2026.

Why Standalone Banking Apps Are Becoming Obsolete

Banking apps solved one problem: digital access.

But they created new friction:

- App switching

- Login fatigue

- Complex navigation

- Form-based transfers

- Slow international processing

- Disconnected financial insights

Users don’t think in dashboards.

They think in intent.

“I need to pay someone.”

“I need to split a bill.”

“I need to move money.”

“I need to understand this charge.”

The future of finance aligns with human behaviour, not software architecture.

That’s why chat-based banking is replacing app-based banking.

The Messaging Platform Takeover

Messaging platforms are now the most used digital environments globally.

People spend hours daily inside:

- WhatsApp

- Telegram

- iMessage

- AI assistants

Finance moving into these platforms was inevitable.

Embedded payments in 2026 allow users to:

- Send money within chats

- Receive funds instantly

- Confirm transactions conversationally

- Get real-time explanations from AI

When finance lives where communication already happens, friction disappears.

And when friction disappears, adoption explodes.

The Psychology Behind Invisible Finance

There’s a deeper shift happening.

Apps require deliberate action.

Invisible systems respond to natural behaviour.

Instead of:

- Deciding to open an app

- Navigating menus

- Filling out forms

You simply express intent.

The system handles the complexity.

This reduces:

- Cognitive load

- Financial anxiety

- Technical intimidation

- User error

Invisible finance is not just a UX improvement. It’s a behavioural redesign.

Embedded Payments 2026: The Infrastructure Shift

Embedded payments are no longer a feature.

They are infrastructure.

In 2026, businesses, creators, and individuals expect payments to happen instantly within:

- Marketplaces

- Social platforms

- Messaging apps

- AI-driven ecosystems

Standalone banking apps now feel like going to a physical branch in 2010.

Functional but outdated.

The winners of this era are not building better apps; they are embedding finance invisibly into existing digital flows.

The Role of AI in the Chat-Based Banking Future

Artificial intelligence is the catalyst behind invisible finance.

Why?

Because AI understands intent.

When you type:

“Can I afford this?”

“Why was this fee charged?”

“Send money when gas fees drop.”

An AI-powered financial layer can:

- Interpret the request

- Analyse account conditions

- Execute securely

- Explain in plain language

Finance becomes conversational.

And conversations are natural.

This is the foundation of chat-based banking in 2026.

Why RUTO Represents the Next Layer of Invisible Infrastructure

RUTO was not designed as another app.

It was designed as an infrastructure for conversation.

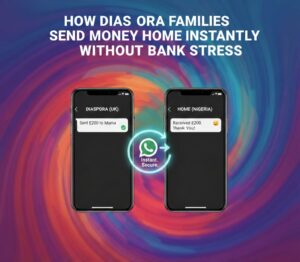

Instead of downloading, registering, navigating, and managing seed phrases, users interact naturally through messaging platforms like WhatsApp.

RUTO enables:

- Instant global payments

- AI-guided financial explanations

- Proactive fee optimization alerts

- Cross-border transfers without banking forms

- Secure identity-based access without seed phrases

This is invisible finance in action.

You don’t open RUTO.

You talk.

And money moves.

From Interfaces to Intent

The evolution of fintech can be summarised in three phases:

Phase 1: Physical Banking

Branches. Paper forms. Waiting lines.

Phase 2: Digital Banking Apps

Mobile apps. Online dashboards. Digital forms.

Phase 3: Invisible Finance

Chat-based execution. AI-driven automation. Embedded payments.

We are now firmly in Phase 3.

The interface is dissolving.

The command line is becoming human language.

Why This Matters for the Next Billion Users

The next billion users will not be onboarded through:

- Complex crypto wallets

- Traditional bank branches

- Technical financial dashboards

They will onboard through platforms they already use daily.

Messaging apps are universal. Chat is intuitive. Conversation requires no tutorial.

Invisible finance lowers the barrier to entry for:

- Diaspora families sending remittances

- Freelancers receiving global payments

- Small businesses paying remote teams

- First-time crypto users

- Emerging market entrepreneurs

When finance becomes embedded, access becomes universal.

The Competitive Advantage of Being Invisible

Here’s the paradox:

The most powerful infrastructure is the least visible. Electricity works because you don’t think about it. The internet works because it disappears behind interfaces.

Finance in 2026 works best when it is not experienced as “finance”.

RUTO’s advantage lies in:

- Reducing visible complexity

- Removing technical friction

- Operating inside existing behaviour loops

- Prioritising human language over financial jargon

Invisibility is not minimalism; it is sophistication layered beneath simplicity.

Fintech Trends 2026: Where This Is Heading

Key fintech trends shaping invisible finance include:

- AI-native financial systems

- Messaging-based transaction layers

- Identity-backed cryptographic security

- Proactive fee optimisation

- Context-aware financial insights

Traditional apps will not vanish overnight.

But they will become secondary layers, fallback systems rather than primary interfaces.

The primary interface will be conversation.

Security in an Invisible World

A natural question arises:

If finance is invisible, is it less secure?

The opposite is true.

Modern invisible systems rely on:

- Device-level authentication

- Multi-factor identity layers

- Behavioural anomaly detection

- Distributed cryptographic security

- AI-powered fraud monitoring

Security becomes stronger because it operates continuously, not just at login.

Invisible finance does not remove safeguards; it removes friction.

The Death of the Finance Dashboard

Dashboards made sense when users needed manual control.

But AI reduces the need for manual oversight.

Instead of reviewing charts and balances daily, users receive:

- Smart alerts

- Spending insights

- Fee timing recommendations

- Risk warnings

Finance becomes proactive instead of reactive.

The app screen becomes optional.

The Bigger Vision: Finance as a Background Layer

The ultimate goal of invisible finance is simple:

Money should move as easily as messages.

No forms.

No switching apps.

No waiting days.

No confusing interfaces.

Just intent.

Execution. Confirmation.

This is not a design trend; it is an infrastructural evolution.

Why Apps Are Disappearing

Apps are disappearing because they interrupt behaviour.

Invisible finance succeeds because it aligns with behaviour.

Embedded, chat-based systems like RUTO represent the next stage of financial evolution — where banking is no longer a destination but a capability woven into everyday digital life.

In 2026, the best financial interface is no interface at all.

And the platforms that understand this shift will define the next decade of fintech.